The Daily Peg

Why the drive to bring transparency to Britain's offshore financial complex may pose a greater threat to dollar dominance than most realise.

Editorial hello

I’m afraid I wasn’t able to make it over to Money 20/20 this year. The downside is that I will miss the jam-packed stablecoin agenda. This is a shame because all the great and the good of the stablecoin world will be there. (You can check out the stablecoin-themed panels here.)

The upside, however, is that I will have more time on my hands to catch up on analysis and reading. And there’s plenty coming in over the week, not least the cross-party House of Lords Financial Services Regulation Committee report, ‘Stablecoins: waiting for regulation’, which lands overnight.

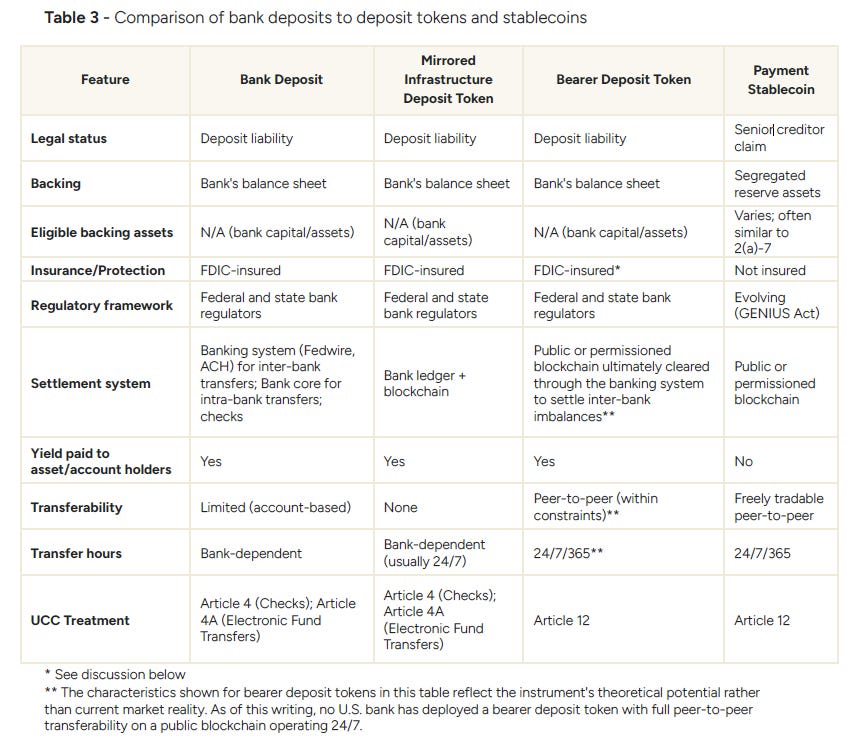

Meanwhile, a fascinating new paper from Omnia Financial, the law firm Hunton Andrews Kurth, and the regulatory advisory firm Klaros Group, Banking Stablecoins: A Regulatory and Operational Framework has also just landed. It is chiefly concerned with how the GENIUS framework will work in practice, especially with respect to capital treatment, liquidity management and operational integration. In that vein, it offers an enlightening analysis of how the regime has created a markedly different creditor hierarchy from that which has traditionally applied to unsecured claimants.

The ramifications of this are deeply under-appreciated by the mainstream media.

According to the report, under the proposed GENIUS regime, reserve assets backing stablecoins would be segregated from the issuer’s bankruptcy estate and held for the benefit of token holders. Stablecoin holders would have first claim on those reserves, with distributions made on a pro-rata basis. However, if those reserves proved insufficient, any remaining claims would receive a super-priority treatment ranking ahead of ordinary unsecured creditors and even ahead of administrative expenses incurred during bankruptcy proceedings.

But it’s also the case that the authors stop well short of treating these protections as settled. The report repeatedly acknowledges that the practical operation of the proposed waterfall remains untested. In particular, it highlights concerns raised by commentators regarding competing secured claims, the adequacy of reserve segregation arrangements prior to insolvency, and the treatment of debtor-in-possession financing. The latter is especially important because Chapter 11 restructurings typically require new financing from lenders who demand super-priority status. Whether such lenders could obtain claims over supposedly ring-fenced reserve assets remains unresolved.

It all, frankly, points to a potential mess regarding future bank resolution.

The authors also identify a more fundamental tension. If reserve assets are excluded from the bankruptcy estate and reserved exclusively for token holders, questions arise about how the insolvency process itself would be funded. Bankruptcy administrations require lawyers, liquidators, custodians and other professionals, all of whom expect payment. The report notes that regulators may ultimately need to address this issue through additional capital buffers, reserve requirements or segregation controls.

The result is a somewhat paradoxical conclusion. On paper, stablecoin holders appear to enjoy a stronger position than traditional unsecured creditors and potentially stronger protections than many investors in money market products. In practice, however, the report suggests that no one yet knows how these protections would perform in a major issuer failure. The legal architecture is increasingly clear; the real-world insolvency treatment remains largely untested. As stablecoins evolve into an increasingly important vehicle for global dollar circulation, this question of creditor priority may prove one of the most consequential unresolved issues in the entire sector.

We have more on the report below. And much more beyond that.