The Daily Peg

Central bankers fret over stablecoin seigniorage effects, and the UAE signals its dollar-peg may be coming under stress due to the Iran crisis.

Editorial hello

In today’s Daily Peg, BIS boss Pablo Hernandez de Cos warns that stablecoins, rather than increasing fiscal capacity, could constrain it by transferring seigniorage proceeds from the public sector to the private sector.

The warning comes via a speech that was circulated to journalists on an embargoed basis over the weekend, usually a strong signal that its underlying theme is something the BIS is keen on amplifying far and wide. And indeed, the FT’s Martin Arnold has willingly obliged.

I can’t remember who it was exactly who recently quibbled with my framing that stablecoins intrinsically affect how seigniorage is shared across the monetary system. But, whoever it was, thanks to de Cos, I am now vindicated in that assessment. Not that the argument is new. A very similar argument was made by Armstrong and Snower in November 2025 in Project Syndicate (neither of whom are cited by de Cos, FWIW). We wrote that up here.

Beyond that, the WSJ reports that the UAE has inquired about accessing U.S. swap lines, which implies its dollar peg might be facing stress due to reduced dollar inflows on account of the Hormuz crisis. And US senators are not that keen on ‘Gaza coin’.

We’re also revisiting a few items we missed last week, including the testimonies of Economic Secretary to the Treasury Lucy Rigby and FCA payments boss, David Geale, to the House of Lords Financial Services Regulation Committee, in which the officials set out how a major strategic goal of UK stablecoin policy is establishing a flourishing, GBP-denominated stablecoin market.

Industry news

Circle Rolls Out USDC Bridge For Native Cross-Chain Stablecoin Transfers

Regulation

ICYMI: UK House Of Lords Heard from FCA and Economic Secretary to Treasury on Stablecoin Growth And Regulation

https://parliamentlive.tv/Event/Index/6fa41318-da1a-4457-be33-acf0860a50cc#player-tabs

Meeting Synopsis: Economic Secretary to the Treasury, Lucy Rigby KC MP, emphasized that while stablecoins could offer benefits, widespread adoption without the right regulation poses significant risks to financial stability. Rigby also noted that the Treasury recognizes the link between stablecoin growth and increased demand for short-term UK government debt (T-bills), which prompted a recent consultation on the T-bill market.

To manage these risks, Rigby outlined a dual regulatory framework: the Financial Conduct Authority (FCA) will supervise non-systemic stablecoins, while the Bank of England will prudentially regulate “systemic” stablecoins. She explained that the Treasury will determine whether a stablecoin is systemic under the Banking Act 2009 by assessing if disruption to its services could threaten the stability of or confidence in the UK financial system. Treasury officials assisting the Minister added that this high threshold is evaluated based on the coin’s value, service nature, substitutability, and interconnectedness with other coins. To further mitigate financial stability risks, the Treasury official confirmed the Bank of England proposed that systemic stablecoins be backed by a 60/40 split: 60% in short-term government debt and 40% in unremunerated central bank reserves.

Rigby also stated that the primary concern behind the Bank of England’s proposed holding limits is to mitigate “disintermediation”—the risk of consumers moving their money away from commercial bank deposits and into stablecoins.

When Lord Griffith questioned whether the Prudential Regulation Authority (PRA) was overregulating by prohibiting banks from engaging directly in stablecoin business, Rigby defended the rule. She argued it ensures clear consumer protection and distinct product branding, noting that banking groups can still participate if they use separate, insolvency-remote entities. Furthermore, regarding the prohibition of paying interest to stablecoin consumers, Rigby noted this approach aligns with other global jurisdictions. David Geale, the FCA’s Executive Director of Payments, added that the FCA views stablecoins as a means of payment rather than an investment that would yield interest.

Critically, Rigby stated that embracing digital assets is critical to maintaining the UK’s competitive edge and sovereignty as a world-leading financial services hub. A major strategic goal she outlined is establishing a flourishing, GBP-denominated stablecoin market. By leveraging the British Pound’s status as the fourth-largest global FX reserve currency, Rigby argued there is a credible basis for a domestic stablecoin to gain significant global traction, allowing businesses to settle programmable transactions 24/7 and bypass traditional foreign exchange fees.

Lord Holmes Expresses Concern That Failure To Distinguish Between Stablecoins and Crypto Assets Could Undermine UK’s Digital Asset Ambitions

https://www.linkedin.com/posts/lord-chris-holmes_an-interesting-evidence-session-in-the-uk-ugcPost-7450824864963354626-q14-/?utm_source=share&utm_medium=member_desktop&rcm=ACoAAAE5GgYBwG4i-0335jsQ7wmmx40pdF2RP5A

“My fear is that without distinguishing between stablecoins and cryptoassets then firms will face regulatory hurdles simply for using stablecoins instead of cash. It will be more likely that they won’t use them, and without stablecoins, the UK’s wider digital asset ambitions will struggle to get off the ground.”

Lord Holmes, April 17

Bankers Group Rejects White House Stablecoin Report As Wrong Question

The American Bankers Association dismissed a White House report claiming that banning stablecoin yield would only modestly boost bank lending, arguing instead that allowing yields could trigger deposit flight, raise funding costs, and hurt community bank lending.

https://finance.yahoo.com/markets/crypto/articles/wrong-bankers-group-reject-white-131640409.html

Analysis

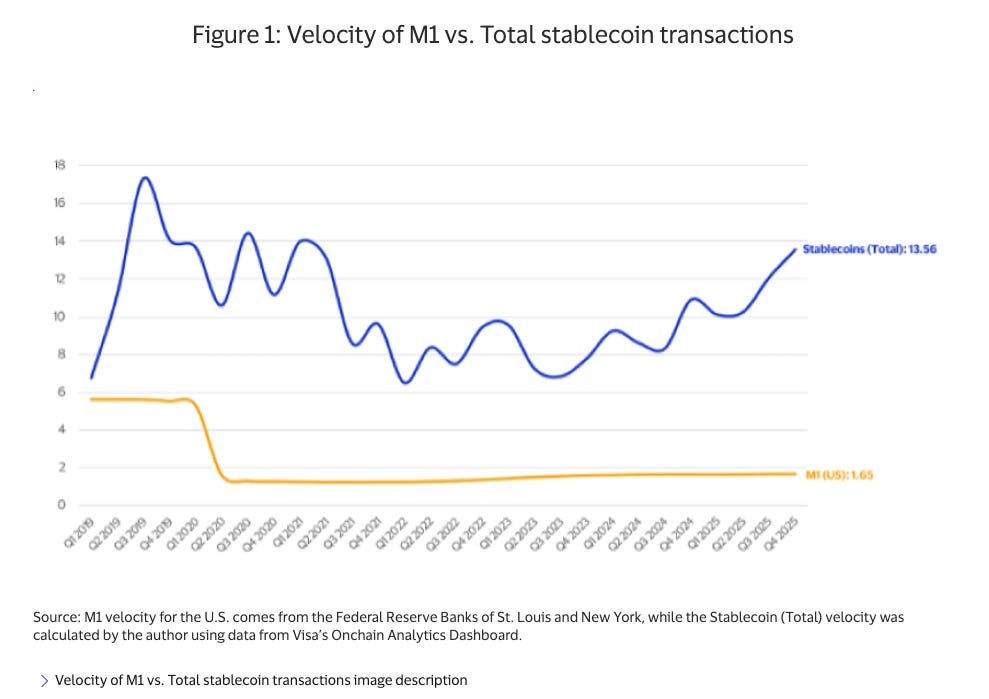

Visa Analysis Finds Stabelcoin Velocity Reached 13.56 in Q4 2025 — Far Above M1 Money Velocity

However, the velocity is driven mainly by financial transactions, with retail velocity at just 0.08 and overall scale still modest versus traditional systems.

https://corporate.visa.com/en/sites/visa-economic-empowerment-institute/stablecoin-velocity.html

ICYMI: HSBC Reserve Managers Skeptical Of Stablecoins Supporting US Dollar Role

https://www.centralbanking.com/central-banks/reserves/7975545/hsbc-reserve-management-trends-2026

“A key tenor of US policy is that stablecoins will drive demand for US Treasuries, thereby supporting the position of the US dollar as the world’s reserve currency. However, central banks on the whole question this assumption, with much depending on developing stablecoin credibility. Of 90 respondents to the question of whether stablecoins would support the role of the USD as a reserve currency, 49 (54.4%) said they are not sure and 27 (30.0%) disagreed. Just 14 (15.6%) said they agree.

In terms of direct exposure to stablecoins and cryptocurrencies, no central banks reported having made any investments, although 6 central banks out of 86 respondents (7.0%) reported considering investing in stablecoins in 5–10 years’ time, and 4 out of 88 central banks (4.5%) said they were considering investing in other cryptocurrencies in that period – compared with 2 saying the same for each asset class last year – signifying a possible small shift sentiment at a minority of institutions.

Just over half of central banks are against a strategic bitcoin reserve fund (53.4% out of 88 respondents), but a significant number (45.5%) are unsure – again, signifying a move towards uncertainty, rather than outright rejection. Last year, 59.5% of 84 respondents were against, and 39.3% were unsure.

Of the 26 central banks that view digital currencies as an increasingly credible asset class, the vast majority (23, or 88.5%) pointed to central bank digital currencies as the preferred choice.”

HSBC Reserve Management Trends 2026, April 8

Institutional Stablecoin Use Tripled In March, with Global Settelemnt Volumes Hitting $584.5 million in March

Deep thoughts

BIS’s De Cos Warns Stablecoins Could Transfer Public Sector Seigniorage to Private Sector

https://www.bis.org/speeches/sp260420.htm

“The increased demand for government debt could lower sovereign borrowing costs, at least at the margin, if stablecoins’ demand for government bonds outweighs the reduction in demand by other market participants. This could increase fiscal space in the near term and is likely to be reinforced when there is foreign demand for domestic currency stablecoins. Such foreign demand could also mitigate the crowding out of credit provision to the private sector induced by flows from bank deposits to stablecoins in the domestic economy.

But there are also ways in which stablecoin use might shrink fiscal space. For instance, to the extent that stablecoins replace cash holdings, seigniorage could shift from the public to the private sector. In addition, the nature of public, permissionless blockchains on which stablecoins circulate opens up new avenues for tax evasion. And runs on stablecoins could trigger forced sales and dislocations in government bond markets.”

Pablo Hernández de Cos, General Manager, Bank for International Settlements, April 20

Institutions Nearing ‘Do Or Die’ Stablecoin Moment Says Bitget Wallet COO

Bitget Wallet COO Alvin Kan warned that institutions face a “do or die” moment and must adopt stablecoins urgently as the market cap surpasses $300 billion and the assets integrate deeper into global payments and traditional finance.

Statecraft

Senators Raise Concerns Over Trump Administration Gaza Stablecoin Proposal

U.S. senators wrote to Secretary Rubio expressing alarm over the proposed U.S. dollar-backed stablecoin for Gaza’s post-war reconstruction, citing risks to the Palestinian financial system, surveillance concerns, ethical issues, and potential conflicts of interest linked to Trump’s crypto ventures.

“We write today to express deep concern regarding reports that the Trump Administration’s ‘Board of Peace’ may develop ‘a US dollar-backed stablecoin for Gaza’ as part of post-war reconstruction efforts. This proposal threatens to undermine the Palestinian financial system, raises significant surveillance and ethical concerns, and creates yet another opportunity for President Trump to promote stablecoin use as his own cryptocurrency company, World Liberty Financial, pushes stablecoin adoption. Therefore, we request information regarding the Administration’s plans to promote the use of a stablecoin in Gaza.”

Senate Letter To Marco Rubio, April 16

French Finance Minister Calls For More Euro-Pegged Stablecoins

UAE Seeks Wartime Dollar Lifeline From Us Amid Middle East Conflict

Emirati officials have asked the U.S. Treasury about a potential currency-swap line to guarantee dollar access if the ongoing Middle East conflict escalates and disrupts the UAE economy.

https://www.wsj.com/world/middle-east/u-a-e-asks-u-s-for-a-wartime-financial-lifeline-3f9ea3a0?

“Emirati officials haven’t made a formal request for a swap line, which would give the U.A.E. central bank inexpensive access to dollars to support its currency or shore up its foreign reserves in case of a liquidity crisis. In talks with the U.S. in recent days, they have portrayed the proposal as preliminary and precautionary, the U.S. officials said.

But they have also argued that it was President Trump’s decision to attack Iran that entangled their country in a destructive conflict whose effects may not be over, some of the officials said. Emirati officials told the U.S. officials that if the U.A.E. runs short of dollars, it may be forced to use Chinese yuan or other countries’ currencies for oil sales and other transactions, some of the officials said.”

WSJ, April 19