Too big to flow: financialisation, fragility and the reserve trap

Why shrinking central bank balance sheets is not an option when financialisation quietly drives every incremental unit of GDP.

This is a guest post by Teodor Kreczmar-Schuldorff, a pseudonym for a European financial plumbing expert who has many deep thoughts about fintech developments but is contractually obliged to repress them for the sake of personal cash flow.

The core contention of this contribution for The Peg, which is based on this unpublished paper, is straightforward, though its implications are not.

Financialisation increases the volume and unpredictability of payment obligations, which requires more liquidity to prevent gridlock — and that liquidity ultimately has to be supplied or backstopped by the central bank.

To unpack that a bit more, as an economy becomes more financialised, the stock of financial assets expands relative to GDP, and the volume of associated cash flows expands with it. Those flows must settle somewhere.

In the United States, they settle predominantly across the Federal Reserve’s wholesale payments system. The underappreciated effect is that financialisation mechanically increases the scale, complexity, and unpredictability of wholesale payment activity.

In essence, a larger and more intricate financial machine requires, by definition, more lubrication. When the lubrication does not keep pace, friction rises, and fragility follows.

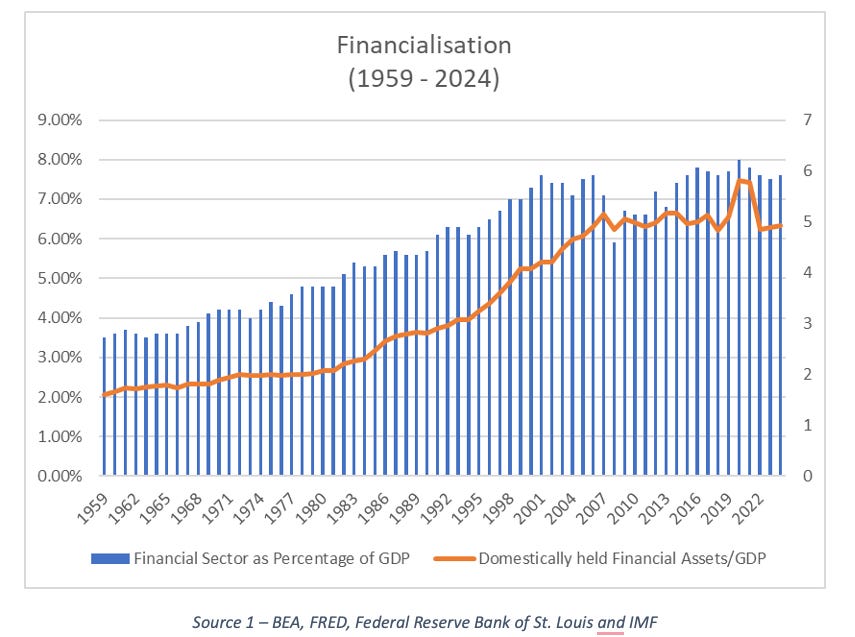

The important context is that since the early 1980s, the United States has experienced a marked and sustained increase in financialisation.

The financial sector’s share of GDP has risen, but more tellingly so has the growth in the ratio of total financial assets to GDP.

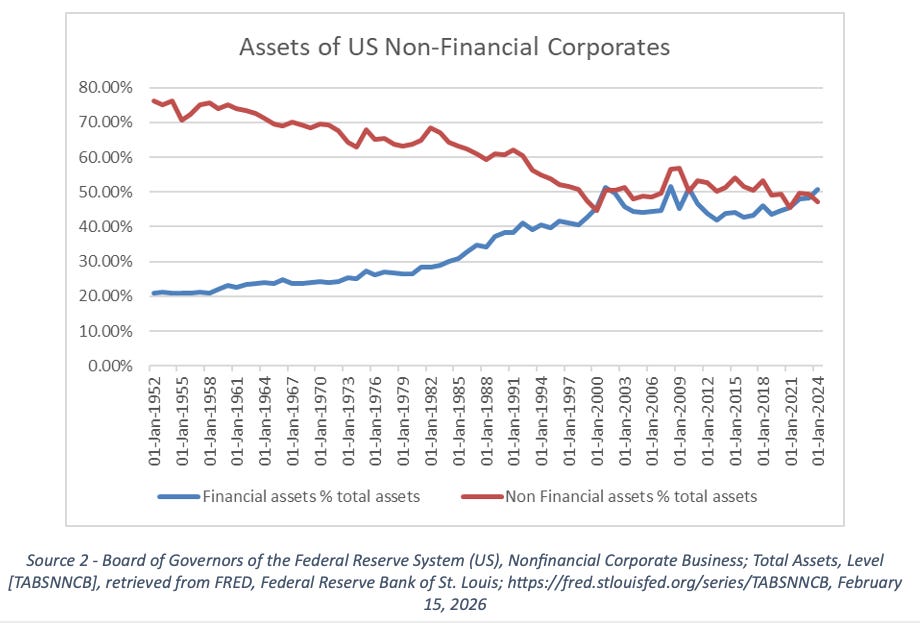

Deregulation, financial innovation, rising public debt, and recurrent asset bubbles have all contributed. Even non-financial corporates now hold balance sheets that are far more financial in character than they were four decades ago.

Furthermore, the growth in derivatives and the globalisation of dollar-denominated assets mean that conventional measures likely understate the true scale of financialisation.

An increase in financial assets is not a passive statistic.

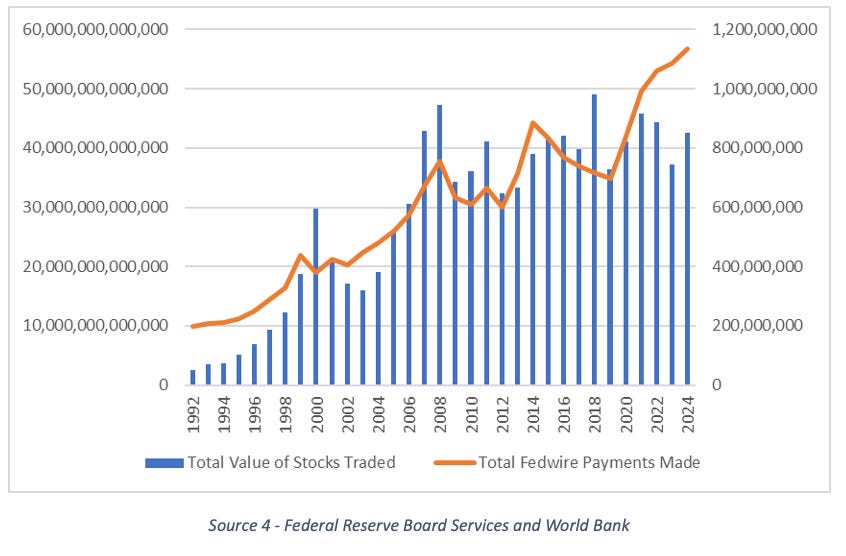

Securities pay coupons, mature, are refinanced, margined, and repoed. Derivatives generate variation margin calls. Asset managers rebalance. Corporates hedge. Banks fund and roll positions. Each of these activities generates payment obligations, many of which are settled through Fedwire.

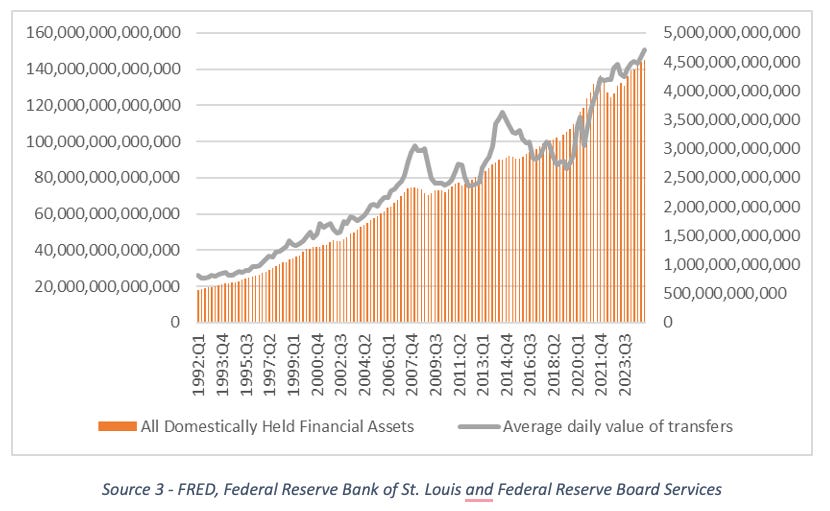

There is, unsurprisingly, a close relationship between the stock of financial assets and the gross value of wholesale payments. The financial system’s arteries seem to thicken as the balance sheet of the economy grows more financial.

As it stands today, wholesale payments are settled in reserve balances held at the Federal Reserve.

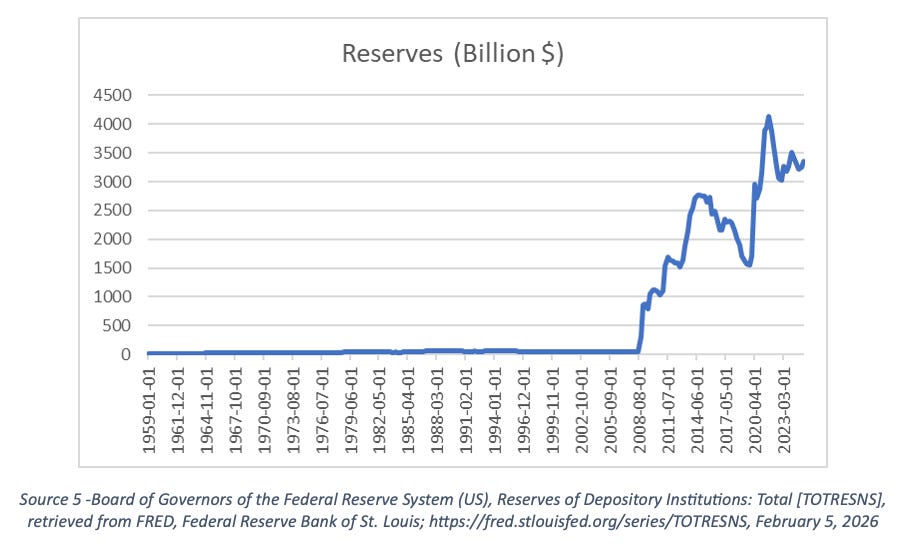

These reserves function as the medium through which banks discharge liabilities to one another. For decades, reserve balances were small and relatively stable. Indeed, prior to 2008, banks had little incentive to hold excess reserves at all, not least because they earned no interest.

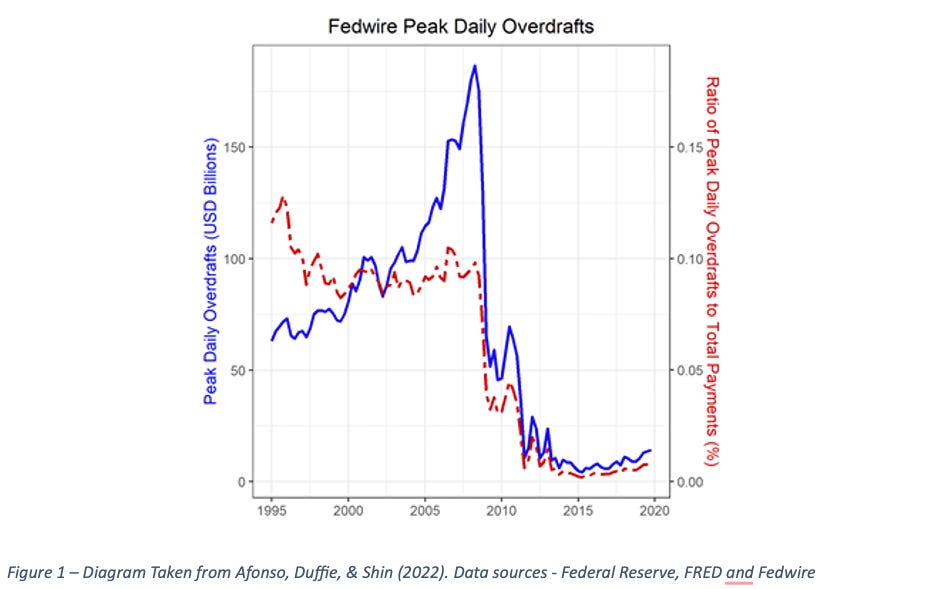

Instead, frictions in intraday payment flows were often addressed through daylight overdrafts provided by the Federal Reserve, as can be seen in the chart below taken from Afonso, Duffie, & Shin (2022).

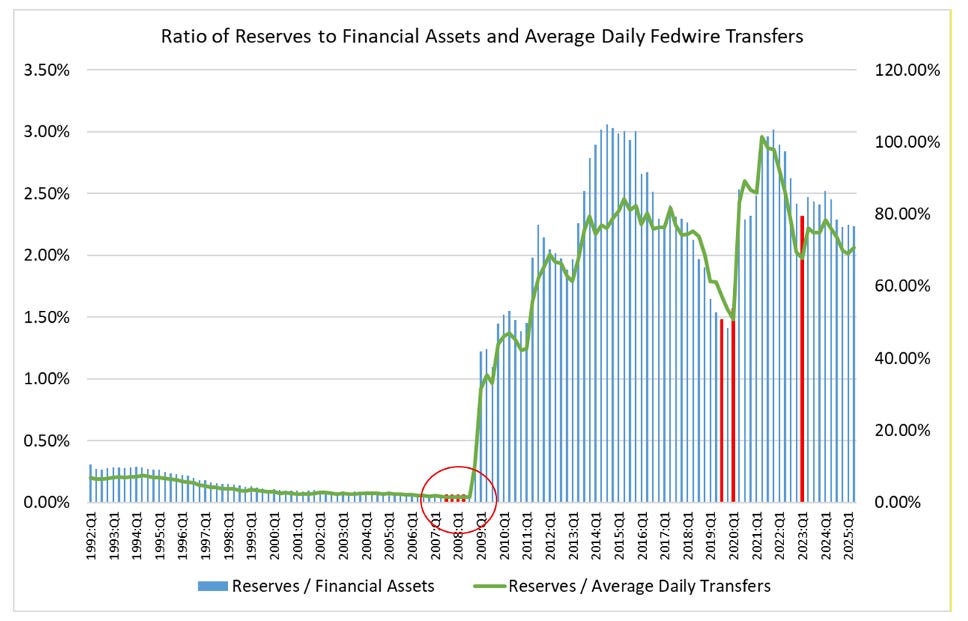

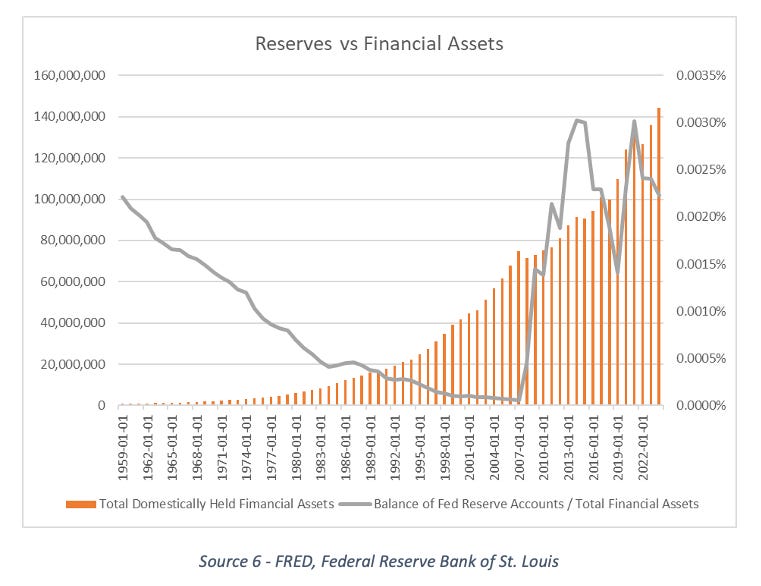

As the system expanded, however, the ratio of reserves to financial assets — and to wholesale payment volumes — declined steadily.

If one views the financial system as a machine, then the 1980s and 1990s saw it grow vastly larger and more complex, with many more moving parts. Yet the quantity of lubrication, measured relative to the machine’s, was falling.

By the mid-2000s, the ratio of reserves to financial assets had reached historic lows. The same was true of reserves relative to average daily Fedwire payments. The system was operating with tighter tolerances and less margin for error.

The global financial crisis did not begin as a payments crisis. It began with a collapse in subprime mortgage valuations and the slow recognition that large quantities of securities were mispriced. Yet the deterioration in reserve ratios preceded the acute phase of the crisis. Liquidity stress intensified as confidence waned. Funding markets seized. Institutions that appeared viable under benign assumptions struggled to finance themselves. The Federal Reserve responded forcefully: policy rates were cut to the effective lower bound, and large-scale asset purchases were initiated. Reserves rose from tens of billions to trillions of dollars within a short period.

The scale of that intervention transformed the operating environment. Excess reserves became abundant. The lubrication problem appeared resolved, at least in the aggregate.

Yet subsequent episodes suggest that the underlying relationship between reserves, financialisation, and fragility did not disappear. In September 2019, repo rates spiked sharply as cash-rich institutions proved unwilling to lend against rising demand for funding. In March 2020, the “dash for cash” saw a disorderly sell-off in US Treasuries and a dramatic expansion of Federal Reserve support. In early 2023, the failure of Silicon Valley Bank and others exposed vulnerabilities linked to maturity transformation and interest rate risk. Each episode followed a period in which reserve ratios had fallen relative to financial assets or payment volumes. Each elicited additional liquidity support.

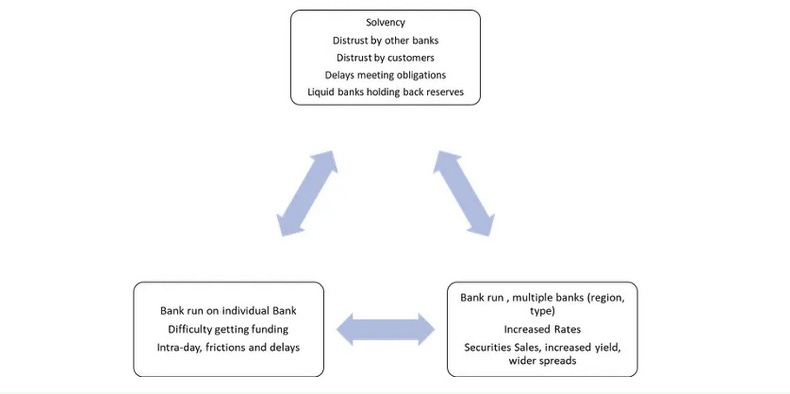

At the same time, it is important to distinguish funding liquidity from market liquidity. Funding liquidity concerns the ability of an institution to meet its obligations when due. Market liquidity concerns the ability to buy or sell assets without materially affecting their price. The two interact. Forced asset sales can depress prices, impair balance sheets, and convert liquidity problems into solvency problems. Conversely, inflated asset prices can mask underlying weakness.

The distinction between solvency and liquidity is conceptually clear but operationally elusive. An institution is insolvent when the fair value of its liabilities exceeds that of its assets. Yet fair value is itself a function of market conditions. A bank may be economically viable over the long term yet technically insolvent at distressed prices. It may also appear solvent in a bubble, sustained by inflated collateral values and cheap funding.

Financial history offers many examples of entities that survived far longer than fundamentals would suggest, supported by financial engineering or outright fraud.

In an environment of persistently high asset prices and abundant liquidity, unviable firms can persist and even expand. They may borrow cheaply against overvalued assets, acquire competitors, and reinforce the cycle. The opportunity cost is borne by the wider economy, which allocates capital to low-return uses.

When central banks respond to stress by lowering rates and injecting reserves, they address immediate funding pressures but may also sustain these dynamics. Yet, treating solvency problems as liquidity problems risks distorting price signals and weakening the market’s capacity to allocate capital efficiently.

The expansion of reserves after 2008, however, reduced friction in wholesale payments and diminished the need for daylight overdrafts.

Yet abundant reserves do not necessarily reside where fragility is greatest. Smaller banks or non-bank intermediaries may hold liquidity claims that are not matched by stable funding. As central banks expand their balance sheets, banks often expand their own, increasing liquidity transformation. When the central bank later attempts to shrink reserves, balance sheets do not always contract symmetrically. The system can become dependent on a high level of aggregate reserves to sustain a given volume of activity, especially when such holdings are regulated into the system for financial stability purposes.

To some degree this is fair enough. Empirical work suggests that lower reserve levels are associated with greater delays in payments and reduced willingness to lend in repo markets. This is consistent with the intuition that less lubrication increases friction. At the same time, high reserve levels may encourage maturity mismatch and leverage.

In reality, the relationship is not linear but cyclical. Falling reserve ratios can heighten the severity of liquidity events. Rising reserves can reduce immediate stress while sowing the seeds of future vulnerability.

The uncomfortable conclusion is that increased financialisation, as measured by the growth of financial assets relative to GDP and payment volumes, increases systemic fragility. The common policy response — lower rates and higher reserves—can mitigate acute funding stress but may entrench structural dependence on abundant liquidity. Over time, the financial system may require ever greater reserve balances to function smoothly, particularly if its scale and complexity continue to expand.

This is problematic since such reserves must, for the most part, be funded at the government’s expense through greater indebtedness.

This leaves central banks with a difficult choice. They may attempt to maintain stability within an increasingly financialised system by supplying ample reserves and intervening decisively during stress. Alternatively, they may consider whether the underlying scale and structure of financial activity should be constrained, accepting that lower reserve levels in a highly financialised system are likely to be associated with greater fragility.

Rolling back decades of financialisation would not be costless, something that is increasingly evident from the Trump administration’s attempt to rebalance the system through tariffs. Yet sustaining it through perpetual liquidity support carries its own risks.

The question is not simply what constitutes the lowest comfortable level of reserves.

It is whether a system built on ever-expanding financial claims can operate safely without continuous and growing central bank lubrication. If liquidity support repeatedly masks solvency issues and mispricing of assets, the long-term damage may outweigh the short-term relief.

The machine can be kept running with more oil, but if obtaining the oil consumes more value than the machine incrementally produces, further enlargement ceases to make economic sense.

The financial system continues amazing me. If anyone has any book recommendations on the subject matter please let me know.